Updates / Essays /

The State's Hand in Space

How targeted government incentives shape the global space industry. Delivered at the Thailand Air and Space Law and Policy Colloquium, Bangkok, 25 February 2026.

In 2006, NASA committed roughly US$800 million to the Commercial Orbital Transportation Services program. The program paid private firms against demonstrated milestones as they developed their own launch vehicles and cargo spacecraft, instead of procuring hardware on traditional contracts. SpaceX built Falcon 9 inside that structure, industrialized production on US$3.1 billion in space station cargo contracts, and brought the price of a launch from about US$150 million to US$67 million. The United States space economy reached US$142.5 billion in 2023.

Commercial activity is now the primary engine of growth in the space economy. The market that activity runs in was built by governments, deliberately, with specific instruments.

Commercial space markets do not form on their own. Space is a high-capital, long-cycle industry with three chronic market failures. Entry costs run to billions of dollars over decade-long timelines. The enabling infrastructure (launch ranges, tracking networks, navigation systems) is a public good no single firm can monetize. And the research spillovers (miniaturized electronics, precision timing, advanced materials) diffuse across the whole economy but cannot be captured by the firm that paid for them. Private capital underinvests in all three, every time. Every commercial space success of this era sits on a state intervention designed to correct that.

The paper behind this essay asks a practical question: which interventions work, which fail, and what a middle-income country should do about it. The evidence comes from seven national programs that produced commercial industries and three that did not.

1. Three levers

Across every successful case, three instruments recur, and they work as one system.

Public R&D builds the technological floor. NASA, ESA, ISRO, and KARI produced the propulsion, avionics, and radiation-hardened electronics that commercial firms later turned into products. The same logic extends to infrastructure. Public test stands, cleanrooms, and tracking networks lower the capital barrier for firms that could never build them alone. ESA’s Business Incubation Centres had supported more than 900 start-ups with a reported 85 percent survival rate as of 2017. NASA’s milestone-based contracting converted public research into commercial capability at roughly one sixth the cost of traditional procurement.

Regulatory clarity makes the sector bankable. The 1984 Commercial Space Launch Act gave American launch operators liability ceilings and a transparent licensing path, which made launch insurable and investable. India created IN-SPACe in 2020 as a single-window authority for private space activity. India had a handful of private space companies in 2019. It now has more than 400.

Anchor tenancy creates the market itself. The state commits to buy a service before a commercial market for that service exists. Structured as fixed-price, milestone-based contracts, the commitment shifts technical risk onto the firm while stabilizing its early cash flow and validating it for investors. COTS and the cargo contracts that followed cut development costs by 30 to 50 percent against traditional procurement. Empirical studies put the downstream multiplier of public space procurement at three to seven dollars per dollar spent.

R&D reduces technical risk. Anchor demand creates the early market. Regulation lets firms scale. Where one lever is missing, the market does not mature.

Each lever also has a known failure mode. Licensing authority dispersed across space, telecom, and defence agencies drives compliance costs up and investment away. Grants and contracts awarded on political rather than performance criteria produce subsidy-dependent firms that cannot compete. Anchor tenancy without a glide path locks firms into government-only demand. The states that managed this well tapered public demand as commercial revenue scaled. They did not withdraw it abruptly.

2. Seven countries

The United States staged its interventions over four decades: federal R&D through the 1960s to 1990s, regulatory liberalization from 1984, then structured demand through COTS in 2006 and Commercial Crew from 2010. SpaceX, ULA, and Rocket Lab scaled inside that sequence.

Europe trades commercial speed for continuity. ESA technology programs run across political cycles, and EU flagships act as multi-decade anchor customers. Copernicus alone carries about €5.8 billion under the 2021-2027 EU space program. The result lags the United States and China on speed and sustains an industrial base that market forces alone would not.

China secured sovereign capability first and opened later. Private entry was permitted only in 2014, under licensing tied to state planning, with demand anchored by state mega-constellations such as Guowang.

India redesigned its institutions instead of building new hardware first. IN-SPACe authorizes private activity and gives firms cost-recovery access to ISRO launchpads, test stands, and ground stations. NSIL, restructured between 2019 and 2022, moves ISRO-developed technology out to private integrators.

South Korea sequenced a complete handover. KSLV-I, from 2002 to 2013, brought propulsion know-how in through partnership. Nuri, from 2010 to 2021, reached roughly 95 percent domestic localization. On 26 November 2025, Nuri flew 13 satellites with Hanwha Aerospace as prime integrator, after a full state-to-industry technology transfer.

Australia built a niche. The 2018 Space Activities Amendment Act made it a predictable jurisdiction for operators, and roughly AUD 200 to 300 million in agency investment supports exportable strengths in space situational awareness, analytics, and ground infrastructure, with little sovereign demand behind them.

The UAE financed national champions: flagship missions from DubaiSat to the Emirates Mars Mission, each with training and technology-transfer clauses written into the contracts, under a unified 2019 space law.

Four patterns hold across all seven. Policy logic sets the tools: security goals drive aggressive R&D, diversification goals support phased liberalization. Institutional structure sets the pace: centralized systems accelerate early capability, hybrid public-private structures sustain commercial growth. Anchor tenancy needs a glide path. And regulatory quality matters more than regulatory model. Predictability and speed determine commercial uptake, not the org chart.

3. The middle-income trap

Middle-income countries fail in a specific, repeating way. Four barriers reinforce each other: sovereign demand too small to anchor a market, attempts at full vertical integration that spread thin resources thinner, institutional fragmentation that no firm can price, and premature liberalization that burns the first generation of companies and the investors behind them.

Escaping the trap means matching the pathway to the country’s actual constraints rather than imitating a high-income model.

Pathway A, the upstream integrator, suits states with large sovereign budgets and security demand: build full domestic launch and manufacturing, and concentrate the transfer on one or two primes. That is Korea.

Pathway B, the balanced dual-track developer, suits mid-to-upper income states with competent institutions: invest across midstream and downstream, buy launch abroad, and support five to seven firms. That is India, which in October 2024 approved a ₹1,000 crore fund, about US$119 million, to accelerate private supply chains while ISRO keeps sovereign launch.

Pathway C, the niche builder, suits states with constrained demand and strong digital sectors: focus on two or three downstream specialists and rely on foreign upstream providers. That is Australia.

4. How states fail

Brazil entered the 2000s with real scientific talent and a working program. Budgets declined through the 2010s. The VLS-1 launcher failed in 1997 and 1999, a pad explosion followed in 2003, and the program was cancelled in 2016. Brazil remains a subsystem supplier to foreign integrators. Public R&D could not compensate for unstable procurement.

Malaysia invested early: MEASAT-1 in 1996, TiungSAT-1 in 2000, RazakSAT in 2009. RazakSAT cost RM 142 million and produced unusable imagery within a year of launch. By 2024 the government had written the operator off, recording losses above RM 112.5 million, and no follow-on mission flew. Early projects without industrial linkages produce project-based operations, not firms.

South Africa built world-class science: the MeerKAT telescope, SUNSAT, SumbandilaSat. SumbandilaSat lost power to radiation damage in 2011 and was retired in 2021. Budget cuts in 2020 and 2021 constrained the agencies behind it, and no follow-on Earth observation mission exists. Scientific excellence dissipates without sustained demand.

The dynamic is the same in all three: discontinuous demand destroys industrial capacity. Space systems need 10 to 15 years of predictable procurement for learning curves to accumulate, specialists to stay, suppliers to survive, and private capital to commit.

5. Thailand’s pathway

Thailand fits Pathway B. The country has competent institutions, an established engineering base, and no near-term requirement for sovereign launch. The framework from the seven cases translates into specific work: publish a credible ten-year sovereign demand schedule covering mixed state and commercial missions, consolidate space licensing into a single predictable window, structure anchor contracts as fixed-price milestones with a planned taper, and size support for five to seven midstream and downstream firms rather than one national champion or twenty grant recipients.

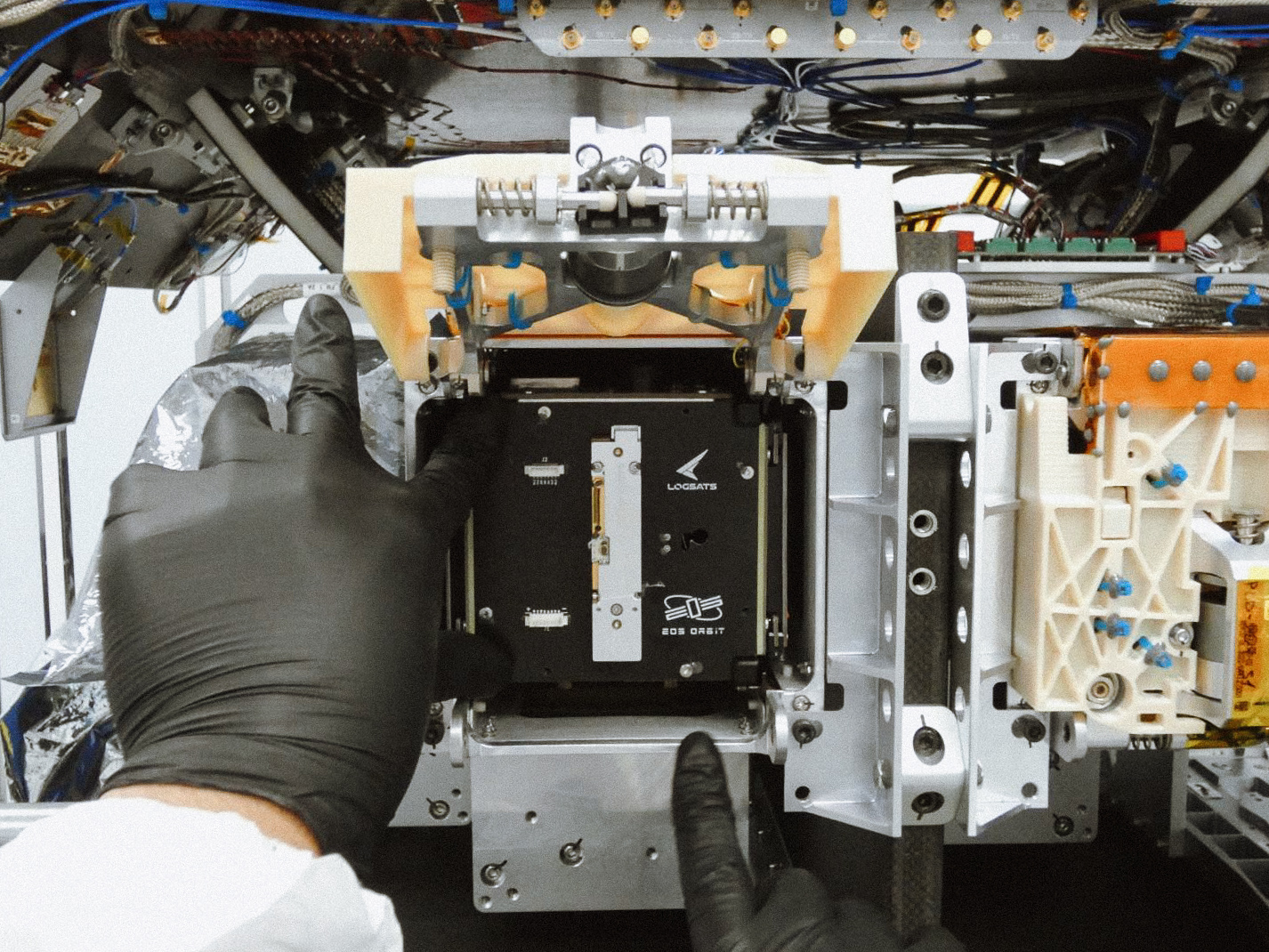

The technical base is not the gap. EOS Orbit, the company I run, designed and built LOGSATS-2 in Bangkok, flew it on a SpaceX Falcon 9 in January 2025, and operated it from our own ground station. The binding constraint on private Thai space capability is now regulatory and demand-side, not technical. That is the correctable kind of constraint. It is the kind India corrected in 2020 and Korea corrected across two decades of sequenced contracts.

Commercial space markets grow where the state provides steady R&D support, simple and predictable rules, and long-term demand. Where rules shift and public investment is inconsistent, strong technical talent does not become a competitive private sector. Brazil, Malaysia, and South Africa show one branch. Korea, India, and Australia show the other. Thailand has not yet published a ten-year demand schedule. That is the place to start.

Adapted from The State’s Hand in Space: How Targeted Government Incentives Drive Success in the Global Space Industry, presented at the Thailand Air and Space Law and Policy Colloquium, Bangkok, 25 February 2026. The full paper is available on request.