Updates / Essays /

The Operator Decade

Thailand has a ten-year window to enter space as a builder. On the category, the operating model that replaced the government program, and the three changes the next decade requires.

Space just became a commercial category. The technology stopped being scarce. The cost stopped being prohibitive. The companies that figured out the new model are now the ones the rest of the industry has to compete with. Thailand has a ten-year window to enter as a builder. We have seen this happen with the internet, with mobile, with AI. The countries that did not start early enough now buy the technology from the ones that did.

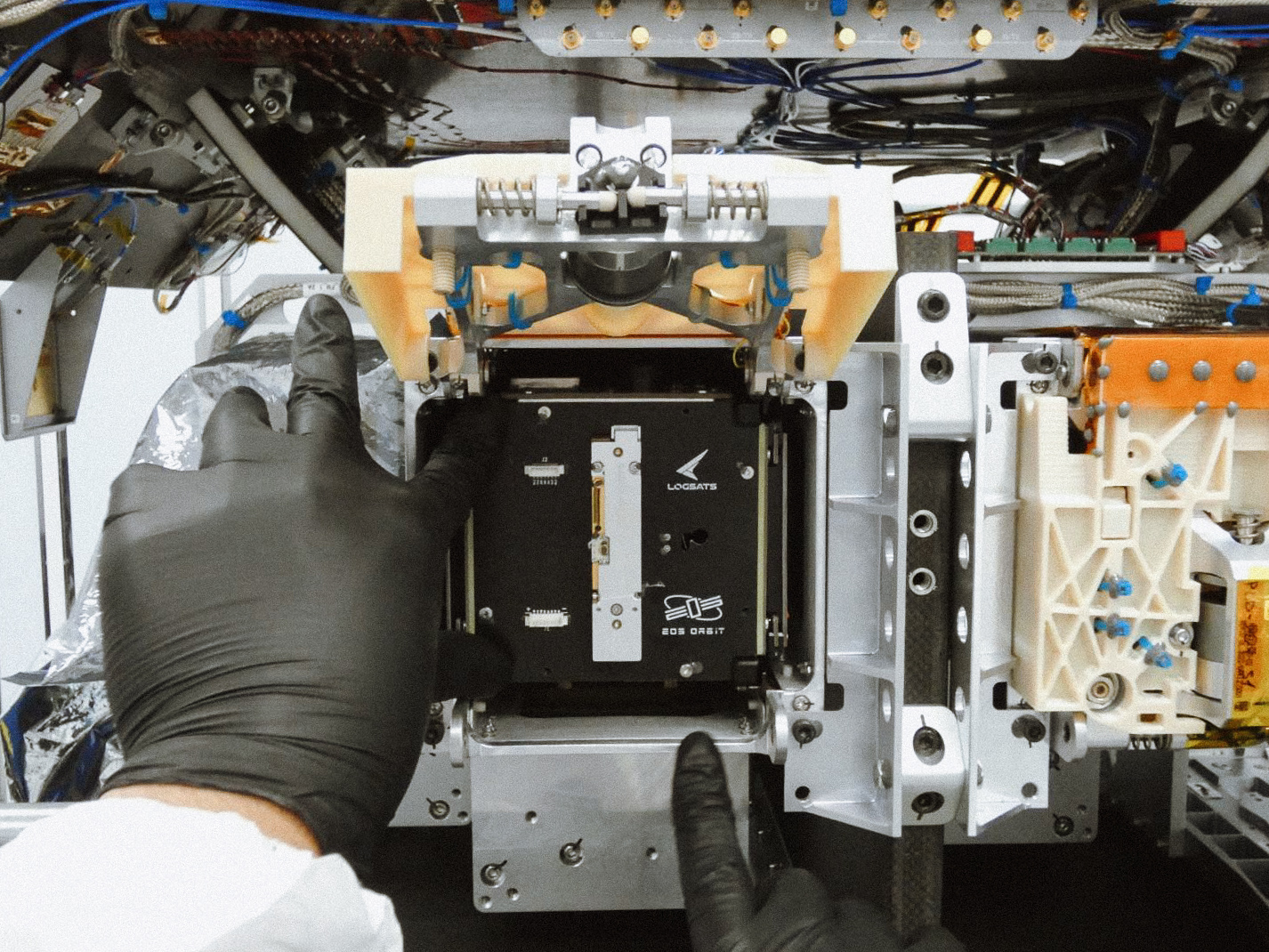

EOS Orbit is one operator inside this category. This essay is about the category, not the company. EOS Orbit is a structural example of what the new model looks like from Thailand.

1. Why now

Many technologies start with wars. Space too. The early Space Race between the United States and the Soviet Union was deeply intertwined with the ICBM race, because the same rocket that could put a satellite into orbit could also deliver a nuclear warhead across continents. Most of the infrastructure of the modern world (GPS, weather imagery, secure communications, intercontinental ballistic capability) came out of that era.

Then the technology becomes mature and enters a more commercial phase. Private companies move faster than governments because they have to. They run out of money if they do not. They lose to competitors if they do not. That pressure is what governments cannot reproduce inside their own budget cycles, and it is what eventually pushes government-built technology toward irrelevance.

Space technology did not move much from Apollo to the early 2000s. NASA spent about $30 billion on the Apollo program through 1975, which RAND has more recently put at roughly $257 billion in 2020 dollars. The Space Shuttle that followed launched 27,500 kg to low Earth orbit at a cost of about $1.5 billion per flight, which works out to roughly $54,500 per kilogram. For four decades that price held. The technology held. Nobody built a different rocket.

Then SpaceX launched the first privately funded liquid-fueled rocket to orbit in 2008. The Falcon 9 today carries 22,800 kg to low Earth orbit at a list price of $67 million per launch, roughly $2,940 per kilogram. The cost dropped by an order of magnitude. The cadence followed: 25 orbital flights in 2020, 31 in 2021, 61 in 2022, 96 in 2023, 134 in 2024, 165 in 2025. The category is no longer a government category that private firms occasionally service. It is a private category that governments occasionally regulate.

In our lifetime we have watched this transition happen with the internet, with mobile phones, with AI. Each had a window when entry was still possible. After the window closed, the countries that did not start became permanent users of someone else’s product. The space window is open now. It will not be open forever.

The operator decade is the ten years between the moment the category proved itself commercial and the moment its winners lock in their positions. We are inside that window. Most of Asia is not yet acting like it.

2. Buyer, not builder

I would not call it wrong. I would say it can be better. The model most of Asia inherited was rational at the time. Most countries built a national space agency in the 1980s or 1990s, modeled on NASA or ESA, with a mandate to operate satellites, train engineers, deliver imagery to the government, and represent the country in international space forums. That made sense. The category was not yet commercial. Private firms could not raise the capital. The agency model was the only model that worked.

During the last 30 to 60 years, the United States sealed the position of leader in many high-tech categories. American technology was usually better. That inevitably pushed Asian countries toward using American technology rather than building their own. We became very familiar with using high technology, and less familiar with building it.

I do not think that is the best way to run a country. In a free and competitive world, too much dependency means too little negotiating power on sovereignty. The countries that broke out of that pattern after the war (Japan from a position much closer to zero than Thailand’s, then Korea, then Taiwan) all did so by becoming builders. They did not stop being users. They added a builder layer underneath. The user layer alone is not a strategy.

Space is not yet owned by any country. I think of the unclaimed orbital and economic territory the way Columbus’s contemporaries thought of the land that later became America. As a government, if you do not start in space, you will lose it to other countries. The land is being divided right now. The fact that the division is happening in low Earth orbit instead of on a continent does not change how permanent the outcome is.

Thailand’s existing national space program is doing the work an agency is supposed to do. It runs satellites, trains engineers, operates ground stations, certifies AIT facilities, and represents Thailand at COPUOS, Artemis, and CEOS. The 2023-2027 strategic plan organizes around four strategies: build the space economy, enhance geoinformatics for national issues, strengthen policy promotion, and transform the organization. The plan’s first space-economy flagship is an “industrial-grade satellite system” with a measurable target of one domestically-designed satellite by 2027, with at least 10 percent of total satellite value sourced from domestic structure or components.

Ten percent is the agency reading of what is achievable inside its own institutional model. It is honest. It is also the number that tells you exactly where the inherited model leaves off. Inside an agency framework, 10 percent is a responsible target. Outside an agency framework, the same satellite class is the entry-level product an operator startup builds at 100 percent before scaling.

The two Earth observation satellites Thailand has flown to date (THEOS-1 and THEOS-2) were built by European primes: EADS Astrium and Airbus. The 100 kg THEOS-2A class is being co-developed with Surrey Satellite Technology in the United Kingdom. The agency is, correctly, treating these programs as technology-transfer opportunities. The transferred capability lands inside the agency. The next step (turning that capability into a portfolio of private operators competing for international customers) is the step the agency model is not structured to take.

The critique is structural, not personal. The people running Thailand’s space program are doing the work an agency is supposed to do. An agency cannot be the operator layer. The operator layer is built by companies that lose money when they fail and capture margin when they succeed. That pressure is what produces the velocity the next decade requires.

3. The cost was cultural

The legacy industry treated space as a category that required a government budget to enter. The new operators figured out that this was a cultural fact, not a technical one.

I feel that if you are given $100 billion to build a rocket, you will use up the $100 billion. If you are given $100 million the way SpaceX started, there is still some chance to build a rocket. It requires dedication, knowledge, and operational discipline that the legacy model never had to develop. The first outside funding into SpaceX was about $20 million from Founders Fund, on top of roughly $100 million that Elon Musk had put in himself. Falcon 1 reached orbit in 2008 after three failed attempts. That is the budget the new model proved was enough. Two orders of magnitude below Apollo.

So funding is not the reason for not doing it. The seed funding for the largest startups in any category (Google, Facebook, the original PayPal that produced Musk’s space capital) always starts small. That is a way of thinking that belongs to startups, not to governments. It is also why startups are the ones pushing technology forward in every category that has matured into a commercial phase.

The numbers carry the argument. Planet operates around 200 satellites and reported $307.7 million in revenue for fiscal year 2026, up 26 percent year over year, with 98 percent of contracts recurring and more than $900 million in backlog. Rocket Lab reported $601.8 million in revenue for fiscal year 2025, split between $199 million in launch services and $402.8 million in space systems, flew 21 missions with 100 percent success, signed more than 30 launch contracts, and closed the year with $1.85 billion in backlog. Electron, Rocket Lab’s small-lift vehicle, is priced at about $7.5 million per dedicated mission. Neutron, the medium-lift vehicle in development, targets about $50 million per launch.

These are not government budgets. They are operating businesses with recurring revenue, multi-year backlog, and capital-efficient infrastructure. Planet’s business is a data subscription business. Rocket Lab’s business is two-thirds satellite systems and one-third launch services. Neither is just a rocket company or just a satellite company. They are operators.

At EOS Orbit, we started with a CubeSat. We would not have started if we did not have a much larger plan attached to it. The CubeSat is the entry-level proof. Equarion is the next satellite. The constellation behind Equarion is the operating asset. We scale when we are ready, not when a budget cycle permits. The discipline forced by a smaller starting point is the discipline that makes the rest of the trajectory possible.

The new operators did not figure out a cheaper way to do the old thing. They figured out that the old thing was set up to be expensive, and that with the right starting constraint a different category of company becomes possible.

4. Three changes

Three things have to change in Thailand’s space policy for the next ten years to look different from the last forty. The decision-makers who can really shape that policy will recognize themselves in what follows.

The first change is the plan itself. Look at China, Korea, India. The governments there have a firm long-range plan to advance technology and to create domestic resources (companies, talent, supply chains) that can build competitive products for the next 10 to 20 years. They do not stop at the products that worked for the last cycle. They do not run the country only on food, agriculture, and tourism. Those continue, but the products are upgraded over time as the world’s standards rise.

Thailand has fallen behind in many of the technologies that defined the last forty years. Internet infrastructure. Mobile. Automobiles. Jet engines. Probably AI. Space is still new. The window is still open. The plan has to put space in the same category as those earlier waves we missed, and decide that this time we enter.

The plan has to be specific. India published its Space Policy in 2023, opened the sector to private players, created IN-SPACe to authorize and guide non-government entities, and created NSIL to commercialize ISRO technology. NSIL has signed roughly 70 technology-transfer agreements moving ISRO-developed capability into industry. In September 2025 the Small Satellite Launch Vehicle was transferred to Hindustan Aeronautics for production. Japan stood up J-SPARC at JAXA in 2018 to co-develop business concepts with private companies, and in 2024 established the Space Strategy Fund at JAXA with 300 billion yen of multi-year support, including 126 billion yen for METI alone. South Korea transferred Nuri launch vehicle technology to Hanwha Aerospace in 2025, in what KASA described as the first complete lifecycle launch-vehicle technology transfer to its private sector. The 2022 base contract was 286 billion won for Nuri improvements and four additional launches through 2027.

What those three governments have in common is not just policy language. It is policy plus procurement plus technology transfer, executed as one mechanism. The agency builds the capability. The agency hands the capability to industry. The agency becomes the anchor customer. The private operator scales. The agency stays as the regulator and as one customer among several.

The second change is the bet. To catch up, there is only one choice, and it is not a government organization. It has to be startups: fast, smart, capital-disciplined, focused on a specific operating asset. The government should promote that layer directly.

Thailand needs at least 10 players in space. Nine will fail. That is correct. The government has to be able to accept this. The model is venture-scale, not procurement-scale. You are not awarding a contract to a known supplier. You are seeding a portfolio and accepting that most of it will not return. The portfolio is judged by what the survivors become, not by the failure rate inside it.

This is a hard frame for governments to absorb. Procurement culture rewards the avoidance of failure. Venture culture rewards exposure to a small number of large successes. The two are not interchangeable. Thailand’s space policy has to be venture-shaped, not procurement-shaped, for the operator layer to exist at all.

Thailand’s national public space investment today is concentrated inside the agency that operates it. GISTDA’s fiscal year 2025 budget is about 1.37 billion baht. Most of that capital is structured to deliver agency-layer outputs: satellite operations, geoinformatics services, training, AIT testing, ground stations. That is appropriate for the agency layer and consistent with the agency’s mandate. The line that would seed a portfolio of ten operator-layer startups at venture scale is not yet sized as ten startups. That is the capital position the next decade has to change.

The third change is the environment around those startups. A startup needs an environment, not just a check. Without the environment, the bottleneck moves outside the startup’s control. Funding is one part. Supporting laws are another. Supply chains are another. The biggest one is talent: enough engineers educated to the right standard, with the right experience, willing to take startup risk inside Thailand.

The environment is what India, Japan, and Korea built. India built IN-SPACe to authorize non-government entities to operate end-to-end space activities. NSIL became the commercial arm that moved ISRO technology out. Japan built J-SPARC to co-develop business cases with private firms, then put a multi-year fund behind the program at the scale serious work requires. Korea built KARI as the technology source and Hanwha as the industrial scale partner, with a contract structure that moved from program participation to full transfer over a few years.

None of those countries built the operator layer first and then tried to retrofit the environment around it. They built the environment as one connected mechanism: policy, procurement, technology transfer, talent pipeline, regulatory clarity. The companies grew inside that environment because the environment was ready before the companies needed it.

Thailand has parts of this environment already. GISTDA’s Space Academy targets 400 additional graduates per year, reaching 2,000 trained people by 2027. The Space Krenovation Park exists. The agency runs an AIT facility. The org chart includes offices for space economy promotion, strategic alliance development, and capacity building. The architecture is partially there.

The missing piece is the operator layer that connects all of these together as customers, suppliers, and growth recipients. The training pipeline is producing engineers. The question is whether the next ten years produce ten companies for those engineers to join, or whether the same engineers leave for opportunities in countries that built the operator layer first.

5. Who has to recognize this

This piece picks a specific fight over who recognizes the category.

The first audience is the Thai government buyer. The space data, ground services, and operational infrastructure Thailand uses today are largely procured from foreign vendors. Some of that procurement is correct. Some of it is reflex. The reflex is what has to change. Government buyers should understand that Thailand needs companies like EOS Orbit to exist, that those companies become viable only when sovereign demand is part of the customer mix, and that the choice to buy domestic is the choice to put the operator layer on the map.

The right feeling for a Thai government buyer who defaults to a foreign vendor is not abstract dissatisfaction. It is the feeling a Korean or Japanese buyer would have had in 1985 if they kept defaulting to American suppliers while their own industrial base was ready to compete. It does not require shouting. It requires recognition. The cost of the reflex is the operator layer.

The second audience is the international customer. EOS Orbit has to be one of the right choices outside Thailand too. The reference I use here is MikroTik. A router company from Latvia. People around the world run their networks on its hardware because it is more customizable than the alternatives, at a better price, with documentation that respects technical buyers. Most users do not know it is Latvian, and the company does not need them to.

Thailand can be that kind of supplier in space. A country that can shake hands with both China and the West. A country whose operating product wins on the technical merit, not on the flag. The question we have to answer for international customers is the same question MikroTik answered: what is the specific feature you cannot get cheaper, faster, or with better fit anywhere else? When EOS Orbit has that answer, the geography of where we are headquartered stops being an objection and starts being a fact.

The third audience is capital. The investors who fund the operator decade are moving now. The ones who think the way Planet’s and Rocket Lab’s backers thought a decade ago will recognize the structure of what EOS Orbit is doing. The ones who still believe the category requires a government balance sheet to enter will not. Both groups are useful to identify. The ones who recognize the structure are the ones we want involved early. The ones who do not will, in five years, find that the bus has left and that catching it on the next route costs more.

There is no version of this where Thailand opts out and another country builds the operator layer for us. There is also no version where one company carries the entire layer. The decade requires a portfolio. EOS Orbit is one example. The country needs at least nine more.

If you are an engineer who has done the work to build operating infrastructure and you want to do it from Thailand, we are hiring. If you are a government partner who can shape the procurement environment so that ten operators are possible, we are open to that conversation. If you are an investor who recognizes the structure, we are talking.

The window is open for the next several years. It will close. The countries and companies that move now will be in the category permanently. The ones that wait will pay to use what others built.

EOS Orbit is building one operator from Thailand. The decade has room for more. Build with us, or build the next one yourself.